Making sense of the National debt can be challenging.

As Congress begins to debate the proposed $2.5 trillion American Jobs Plan, much is being made of the ballooning National debt, which now stands at a whopping $28 trillion dollars. I thought it might be useful to put some facts in context for our readers.

For many years, fear mongering about the country’s debt levels has been a popular tool for politicians on both sides of the aisle. Common talking points include statements like, “We are going to bankrupt the country”, “China is going to call in all our debt and we’ll be in slavery”, and “We’re mortgaging our grandchildren’s future.” I will seek to address how valid (or not) these statements are, how the National debt really works, and how we should think about it going forward.

Most Americans understand little about America’s debt and deficits. So, let’s start with the basics.

The difference between debt and deficits

The federal government receives the most income from federal taxes. Then, the government spends money on things like the military, social programs like Medicare and Social Security, and so on. A country runs a deficit when it spends more money than it brings in annually.

To cover that a deficit, the government “borrows” money, primarily by selling government bonds to whomever wishes to buy them. That creates a debt. So, the deficit is an annual measurement of how much the government needs to borrow. The National debt is the cumulative amount a country owes over time due to annual deficits. Simple enough.

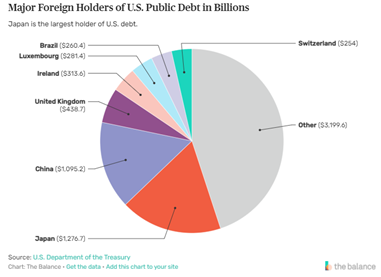

Who actually owns the National debt?

So how much of our debt is really owned by foreign countries? The truth is the majority of public debt is owned by the American people. In fact, 78% of the National Debt is owned by Americans or the US government.

Only 15% is owned by foreign governments. Japan and China, the two governments with the largest share of foreign ownership, both own a little more the $1 trillion dollar. Together, they own about 2% of the total National debt.

Consider this: Social Security, retirement accounts, and pension funds collectively hold about half the National debt on your behalf for retirement.

How much National debt is too much?

“Still”, you say, “$28 trillion in debt cannot be healthy.” In general, we would agree. There are two questions that come to mind to help us make sense of this.

- How much debt is too much?

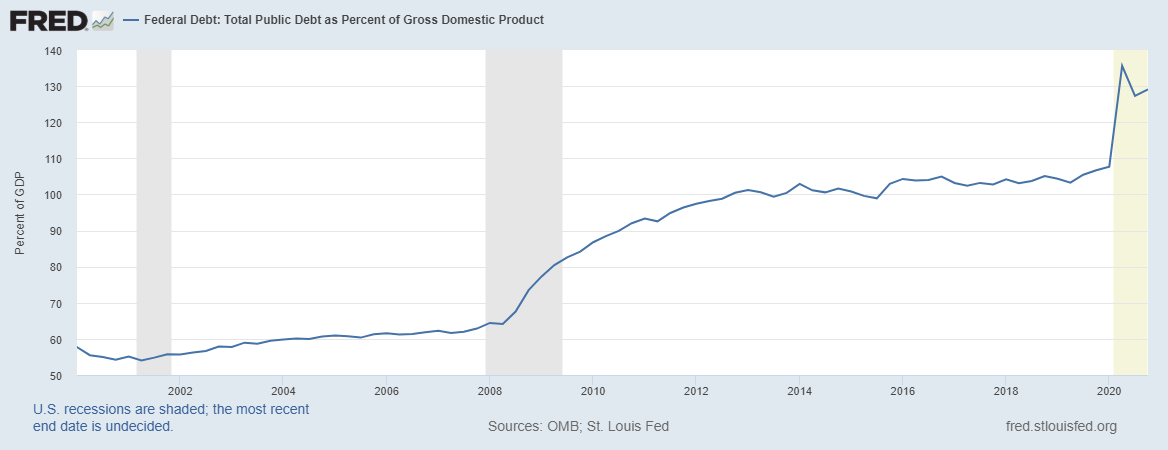

The short answer here is no one really knows. For many years, economists suggested that measuring national debt against annual Gross Domestic Product (all the goods and services produced by the US in a year) was a good yardstick, and that any time the Debt-to-GDP ratio reached 100%, it was a warning sign of imminent financial collapse. Well, guess what? We’ve been at that level since 2012.

Yes, I see the spike on the right side of the chart too. Keep in mind that while GDP fell last year the government was deploying stimulus efforts to stabilize the economic impact of the Covid recession. I suspect as the economy continues to improve through this year, the ratio will begin to stabilize and decrease as GDP growth resumes.

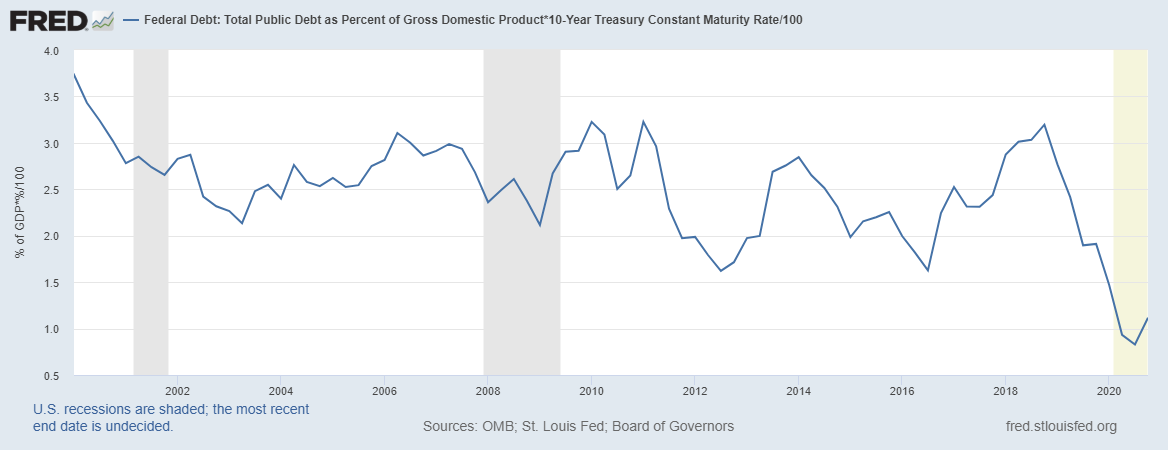

As of late, many economists have changed their thinking about the Debt to GDP yardstick. A popular current line of thinking suggests if the economy grows at a rate that exceeds the interest on the debt, we can come out ahead. Time will tell, but the good news is that the interest paid on the National debt as a percentage of GDP has been in decline for some time.

As the following chart shows, the cost of borrowing has been in decline for two decades and this has made it easier to handle the increasing National debt.

The rational speculation is that sooner or later interest rates will rise and that will increase the cost of all this debt. That is where the problem comes in.

While it is scary to think about having to pay off all that debt, it does not happen all at once. That is not how it works. The currently outstanding debt gets retired over a very long period of time as bonds become due and are redeemed. New bonds are issued all the time, replacing the retiring debt. It’s a perpetual process that runs indefinitely.

I don’t think the size of the debt will become a concern for the markets until interest rates rise sufficiently to increase the borrowing costs to an unsustainable level.

This takes us to question #2.

- Are we just running up debt, or are we getting anything for it in return?

Going into debt can actually be a good thing if you are getting something in return. The question is – are we spending the money on the right things? If you are borrowing money to create real economic activity (jobs, infrastructure, etc.), then borrowing can be a positive.

For example, let’s say you have a great idea for a product and you go to the bank and borrow money to build a factory. That factory will hire people and those employees will spend their money in the local community. That borrowed money will facilitate the creation of create goods that stimulate the economy. These are good things, and they would not have occurred without borrowing. Some extremely valuable companies like Amazon, Tesla, and Apple got that way by borrowing a lot more money than they initially earned. They invested in their future.

A large portion of our current deficits are entitlement programs such as Medicare, Social Security, and more recently enhanced unemployment insurance benefits. We are getting something for the money we are spending – a social safety net.

Borrowing money to invest in infrastructure, social programs, improving schools, advancing technological innovation, and the like are generally investments that pay off down the road. Unfortunately, most large spending bills also contain a lot of pork – a byproduct of our political dysfunction. That’s a subject for another blog.

Borrowing responsibly to invest in future prosperity could be a good thing. Borrowing to fund pet projects and curry favor with large political factions is not. I encourage readers to pay attention and ponder these questions as the current spending bills work their way through Congress, and let your representative know your thoughts.

How the National debt affects your portfolio

From an investor’s point of view, the question you are likely wondering is how the National debt affects your investments. That is a good question. Unfortunately, it is not an easy one to answer. Here are a couple ways I look at it.

First, if the financial markets begin to question the ability of the government to meet their interest obligations, we will see that reflected in the value of government bonds. That might bring a period of volatility to both the stock and bond markets. Compared to how other developed economies around the world are handling their finances, the United States remains the best performer. Despite the recent increase in additional debt, the financial markets continue to favor the U.S. over other countries. I don’t see this changing any time soon.

Second, there is a small risk that the National debt could lead to a structural increase in inflation if the interest costs become onerous. Inflation is influenced by so many different variables and recent history suggests that the size of the National debt has little influence in leading to inflation. The best defense against inflation is a healthy dose of stocks that have the ability to generate strong earnings.

Finally, the persistent demand by investors for bonds will likely continue for a long time, and those investors will be the primary buyer of government bonds. In my opinion, that demand for bonds is a significant reason interest rates will remain relatively low for a long time. (Remember from Economics that demand leads to higher prices. In the case of bonds, higher prices lead to lower interest rates.) If interest rates remain low, the return from that portion of your portfolio will need to be offset by the return on stocks.

In closing

I hope you find this perspective useful. The National debt is generating a lot of conversation, and for good reasons. Its size and influence on the economy is very complex and the long-term impacts are unknown. While I think it deserves attention, I don’t think its size will have a near-term impact of your investments.