As you might imagine, we’ve had a few folks inquiring about the current state of the markets, the outlook for the rest of this year, and what 2023 might have in store. We’ve prepared this summary to give our readers a way to take stock of things and to provide some much-needed perspective. Here we go:

Why is the Federal Reserve raising interest rates?

This is a complex question with lots of moving parts. We’ll do our best to briefly break it down for you.

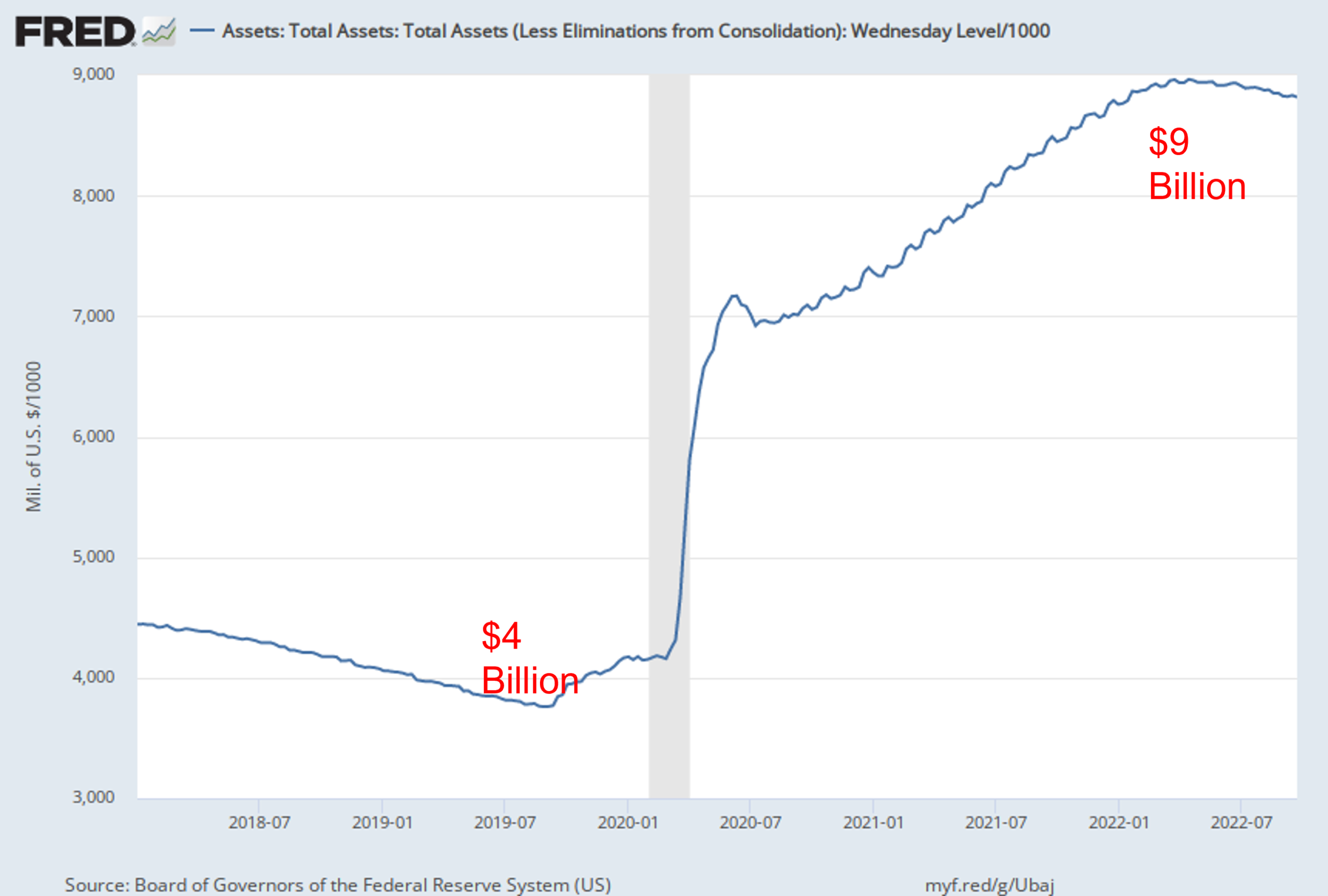

Having some perspective on what got us here in the first place is essential. For that, we’ll need to go back to early 2020, when COVID came to our shores. In response to the global economic shutdown, the Federal Government spent over 6 trillion dollars in the subsequent two years to support the economy. (We won’t get into whether this was right or wrong.) Where did the Government get that money? They issued bonds which the Federal Reserve then promptly bought.

Simultaneously to the Government’s spending initiatives, the Federal Reserve lowered short-term interest rates to zero. Low interest rates spur spending, as evidenced by the massive increase in home buying from the last half of 2020 through earlier this year.

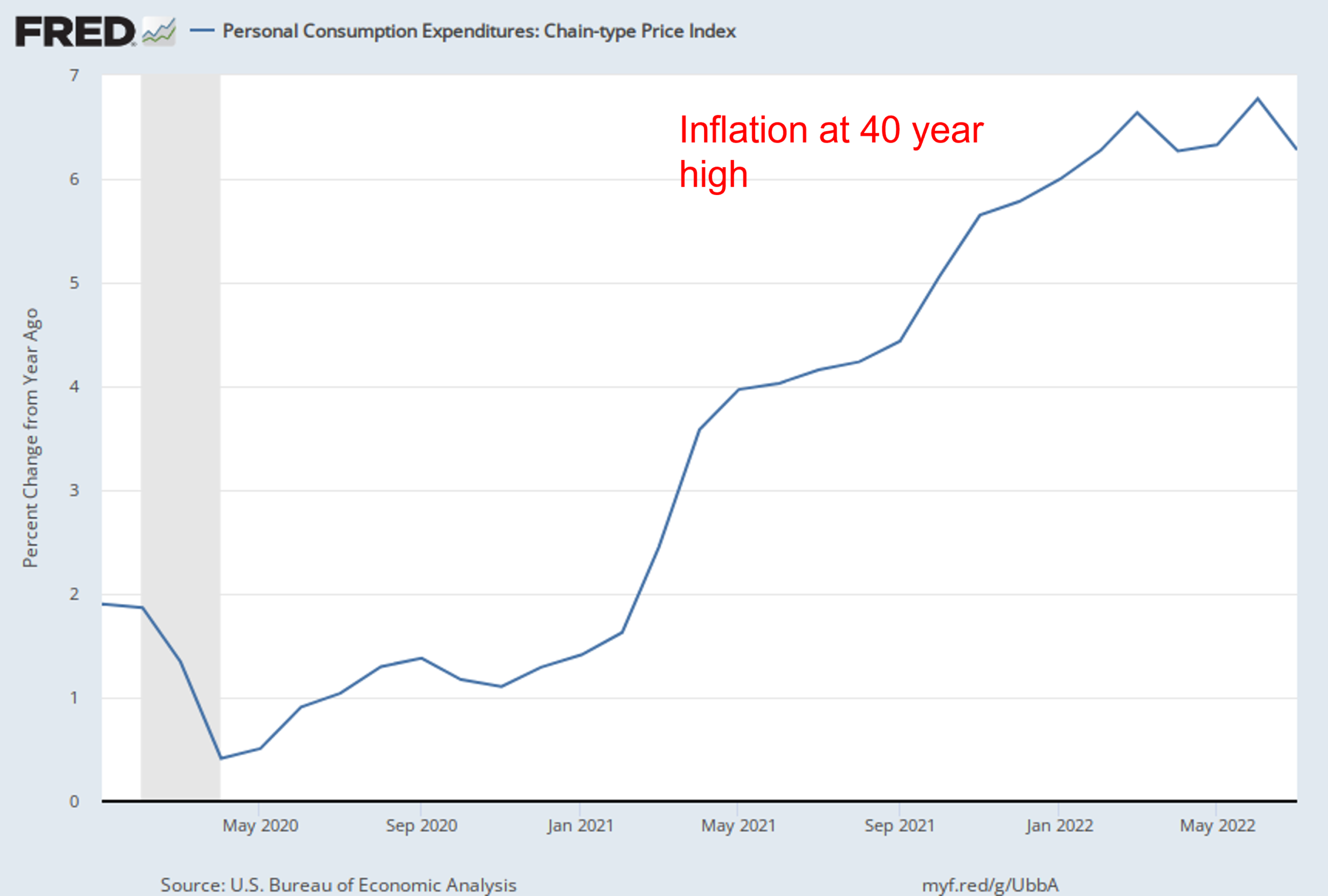

All of this excess liquidity went into the pockets of consumers and companies. As we recovered from COVID, the demand for goods and services far outstripped the supply available. When demand exceeds supply, prices go up, and that’s how you get inflation.

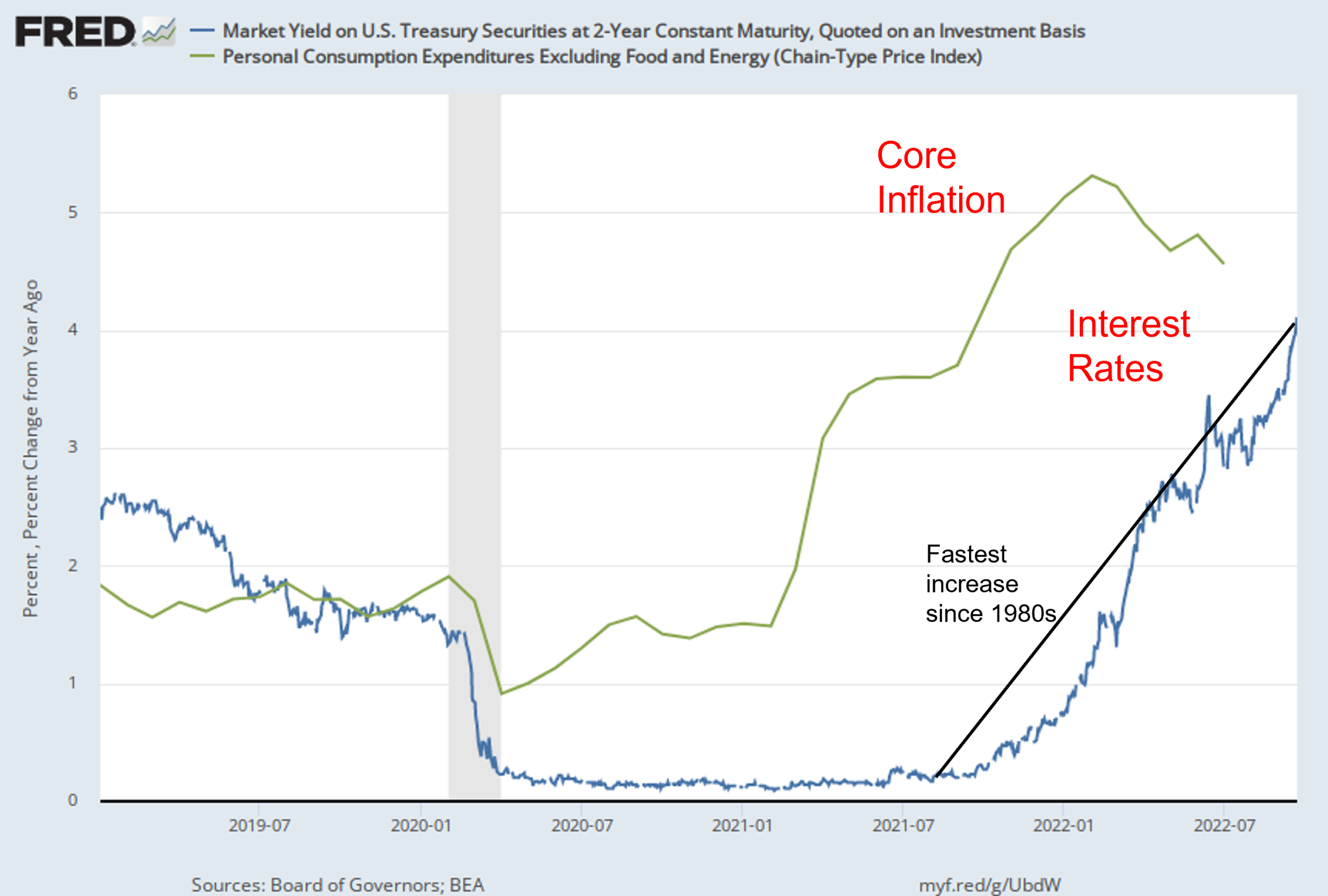

How do you fight inflation? Essentially, by reducing demand. When demand falls, prices typically follow. The Fed raises interest rates to make borrowing more expensive, and companies and consumers alike will reduce their spending when the cost of borrowing gets too high. So far, the Fed has raised interest rates this year from zero to 3.25% and will continue increasing them until demand softens.

Why are the stock and bond markets performing so poorly this year?

The first rule of investing is that capital will always flow where it thinks it can get the best return.

In the 2019 – 2021 window, conditions were favorable for US stock and bond markets. We had low interest rates, growing demand, and robust employment. Capital flowed into US investment markets, driving up their prices. As a result, investors enjoyed above-average returns during those three years.

As inflation took hold in mid-2021, the Fed waited – too long, in my opinion – to begin combating it. The more prolonged inflation is embedded in an economy, the more difficult it is to reduce. As the Fed started to raise interest rates, inflation continued to rise, creating uncertainty regarding how high the Fed will need to raise rates and how long it will take to tame inflation.

As we’ve said many times, markets hate uncertainty. For stocks, higher interest rates mean higher borrowing costs and lower growth prospects for their business as demand softens. For bonds, higher interest rates mean lower values for existing bonds. All of this uncertainty has spread far beyond stocks and bonds. Except for energy, every major global asset class is negative for the year— gold, other commodities, stocks, bonds, you name it. Even cash, when adjusted for inflation, is negative for the year. There has been nowhere to hide the from Fed’s interest rate increases.

There is some good news in all this. For one, corporate earnings have been remarkably resilient throughout 2022, and earnings ultimately determine future stock prices. Companies have healthy cash balances to weather the storm and recover more quickly when this is over. And consumers are in excellent shape regarding both savings and low debt levels. Financially healthy companies and consumers are the formulae for robust economic growth, and this should lead to a healthy recovery once the uncertainty subsides.

Are we headed for a recession (or are we already in one)?

The bar stool definition of a recession is two consecutive quarters of negative GDP growth, but the actual definition requires a broad decline in the economy, which includes employment, wages, and corporate profits. High inflation has resulted in meeting the first definition, but low employment, increasing wages, and the highest corporate profits in history paint a different story.

The funny thing about recessions is that the reporting is backward looking. You never know you were in one until it’s over. Forecasts and predictions for a US recession are all over the map. Some believe we are in one now, and others predict we will be in one in late 2023. The truth is no one knows. We expect we will see a recession sooner or later due to the Fed’s actions but based on the current environment and the health of both companies and consumers. We would expect it to be modest if and when it occurs.

What does all this mean for my investments?

Among other things, Warren Buffet is famous for his saying, “Investing is simple, but not easy.” It isn’t easy to stay the course during challenging times, especially when account values are down. As we noted earlier, capital flows where it believes it will get the best return. Over time, owning a diversified mix of stocks and bonds has provided investors decent risk-adjusted returns to grow their wealth. Once we see inflation decline, the Fed will cease increasing interest rates and will begin to reduce them. When that happens, there’s no better place to be than a quality portfolio of stocks and bonds.

Be patient, exercise discipline, and resist the temptation to “do something” for the sake of doing something. If you have capital to put to work, now would be an excellent time to do so. At the risk of repeating ourselves, remember this well: 100% of the time throughout history, markets have declined, but they have recovered and gone on to new highs. This time will be no different.

What should we do now?

Keep your perspective. If you’ve been a subscriber for a while, you may recall our advice during the height of the COVID panic, when the stock market (as defined by the S&P 500) declined 34% in three painful weeks. If you missed it, here’s the essence of what we wrote during those dark days:

The world is always ending, but it just never ends. There’s always a new crisis to replace the old one. COVID is a virus. And all viruses are ultimately contained or eradicated. This will end. And another world-ending crisis du jour will take its place.

In their 1971 hit “Won’t Get Fooled Again,” the Who prophetically sang, “Meet the new boss, same as the old boss.” The point is – all crises end with a new beginning. Inflation will ultimately roll over and be tamed. America’s greatest companies will get back to the business of making profits for their shareholders. Bond prices will recover. The sun will come out again. The question for investors is, where will you be when it happens?

As always, we’re here for you. Don’t hesitate to pick up the phone and call us if we can offer any advice or guidance.

Be sure to register for our upcoming webinar on October 18th, where we’ll discuss this and our expectations for what is to come.