August marks the point at which we start to make year over year comparisons to the Covid Recovery that began in earnest this time last year. One of the major headlines that has prevailed over the past few months is the thought that inflation will be persistently high going forward. The concern is logical, especially given the latest reading of 5.3%. This headline will continue into next year, so we wanted to provide you with an update on our thoughts on the topic.

We have talked about this a few times this year (here’s an example), but it is worth repeating. If you compare a high number with a low number, the result will be a high number. At this stage in the economic cycle, the increase in inflation we are seeing is more about math than structural changes within the economy. Let me explain.

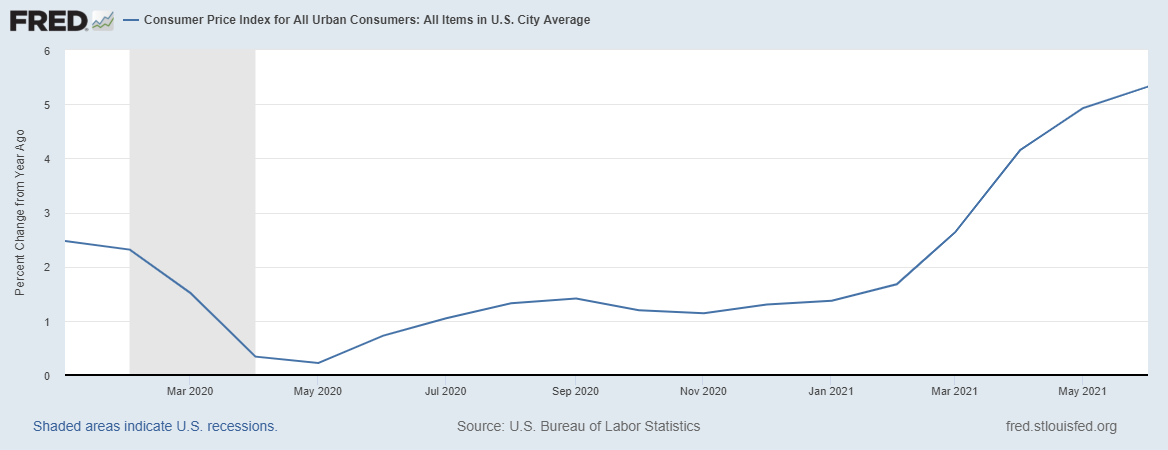

The following graph depicts the rate of change that inflation has experienced since January 2020.

As you can see on the left side of the graph, inflation decelerated as the economy came to a near-halt at the start of the Covid experience in March a year ago. This means prices declined, especially in the energy and transportation sectors. As the economy reopened and accelerated, prices began to recover, and in some cases exceed their previous levels.

Products that have seen their prices increase the most are driven by supply constraints more than anything else. You may be familiar with the narrative surrounding the lack of computer chips used in the manufacture of cars. Car companies, at the start of the pandemic reduced their orders for these components because they didn’t think people would want to buy cars in the midst of Covid. Computer chip suppliers shifted their production capacity to other customers and the car companies gave up their spot in line. Unfortunately, the car companies were wrong about customer’s not wanting to buy cars during a pandemic. And that led to people buying used cars instead of new ones – driving the price of used cars through the proverbial roof.

Similar stories played out throughout the economy as production stopped at the start of the pandemic and then restarted later in the year.

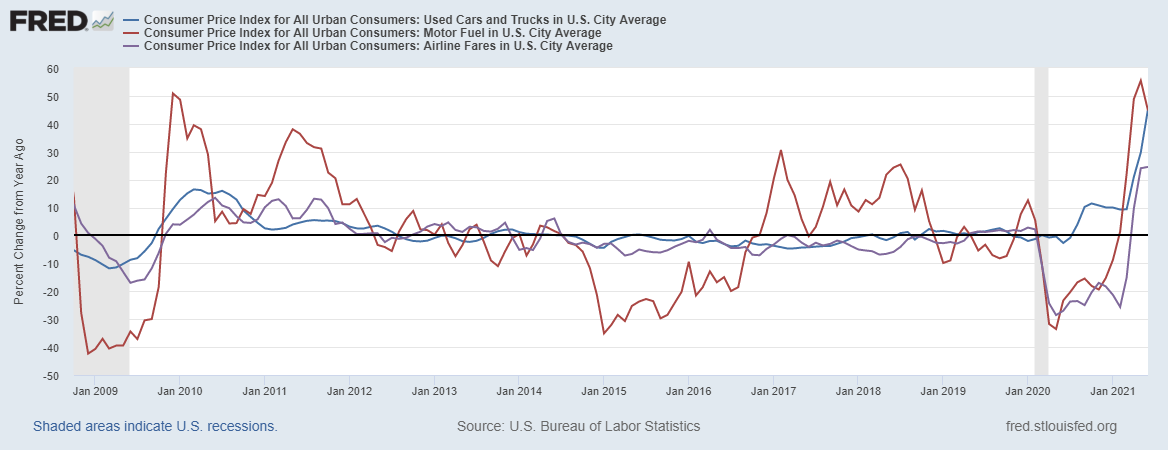

The two primary contributors to why the rate of inflation has accelerated over the past few months are the increase in the price of used cars and the recovery in the price of gasoline. The following graph depicts the magnitude of these components.

Let’s start by looking at the right side of the graph.

The blue line is the price of used cars. Thanks to the computer chip shortage suppressing the number of new cars being produced, the value of used cars increased a rate never before seen. Yes, that’s more than 40% more than a year ago. You can also see their prices never really decreased during Covid.

The black line is the price of airfares. Note how they declined by nearly 30% during the onset of the pandemic. That’s because air travel almost stopped entirely. We were watching this at the time and a round trip ticket between New York City and Orlando could be had for as little as $60. Yes – $60 dollars. Now that planes are flying again, airfares have recovered to the former level. The bounce back has been swift and that swiftness has amplified the comparison to the prior period.

The red line is the price of gasoline. Similar to airfare, gas prices fell more than 30% during Covid. In fact, there were a few days early on when the price of oil actually turned negative. Suppliers were willing to pay you to take oil of their hands. If we could only turn back time… Prices for gasoline have recovered and gone on to new highs because supply has not fully returned. This is partly because of political policies, but mostly because producers are being prudent with their production.

Now, take a look at the left side of the graph. We saw similar dynamics play out during the 2008 recession and recovery, although the magnitude was not as strong. And then the rate of inflation moderated as time passed.

If you strip out used cars, gasoline, and airfares inflation is running closer to 2%. Far below the 5.3% headline print.

Take away: the spike we are seeing is normal following a recession.

So, back to the question of whether the increase in inflation is a temporary phenomenon or a structural change?

We continue to think the spike in inflation is temporary. Eventually, inflation will moderate as the year over year comparisons become normalized. It will take several more months for that to happen, and the inflation rate might actually increase before peaking. We are not seeing broad-based increases across the board that would lead us to be concerned at this point in time. So far, it’s been these three components driving the numbers. Eventually they will work themselves out. We’ll continue to monitor this of course and let you know if things change.

In closing, there are a couple points we would like to make about how to use this information.

First, the markets feel the same way we do and they’ve already priced in the effects of temporary higher inflation. The bond market has seen interest rates fall from their early year highs. 10 year government bonds are yielding about 1.25%, down about .5% over the past four months. The stock market is also reading this a temporary and fears of sudden increases in interest rates have abated. As such, portfolios are positioned to navigate through this dynamic. Should inflation persist, the best defense is a healthy allocation to stocks.

Second, discussions about inflation can often get political, especially as we head toward an election cycle. This time is no different. As we mentioned above, it is entirely possible that the headline print for inflation will rise more before peaking. This will make for political dialogue in the media. As we so often do with political topics, we encourage you to keep politics out of your portfolio. Be mindful that the details underpinning inflation are more nuanced than the headline.

Until next time…

By the way, we recently published an article discussing crypto. After receiving numerous questions from clients about crypto, digital currencies and Bitcoin, we though it was time to develop some education material on the topic. The first article in this series focuses on what crypto is and where it came from. Future articles will discuss the tech supporting the concept, along with examples of applications and concepts. If you haven’t seen the article yet, you can read it here.