4 years

That’s how long it’s been since we’ve had a normal environment for investing. It’s hard to believe it’s been that long, but considering everything we’ve been through, I wouldn’t argue that it feels longer for you. In December of 2019, our economy had been in expansion mode for nearly eleven years, one of the longest periods of growth on record. Inflation was averaging less than 1.5% per year. Interest rates on savings and investments were even lower. Then Covid happened.

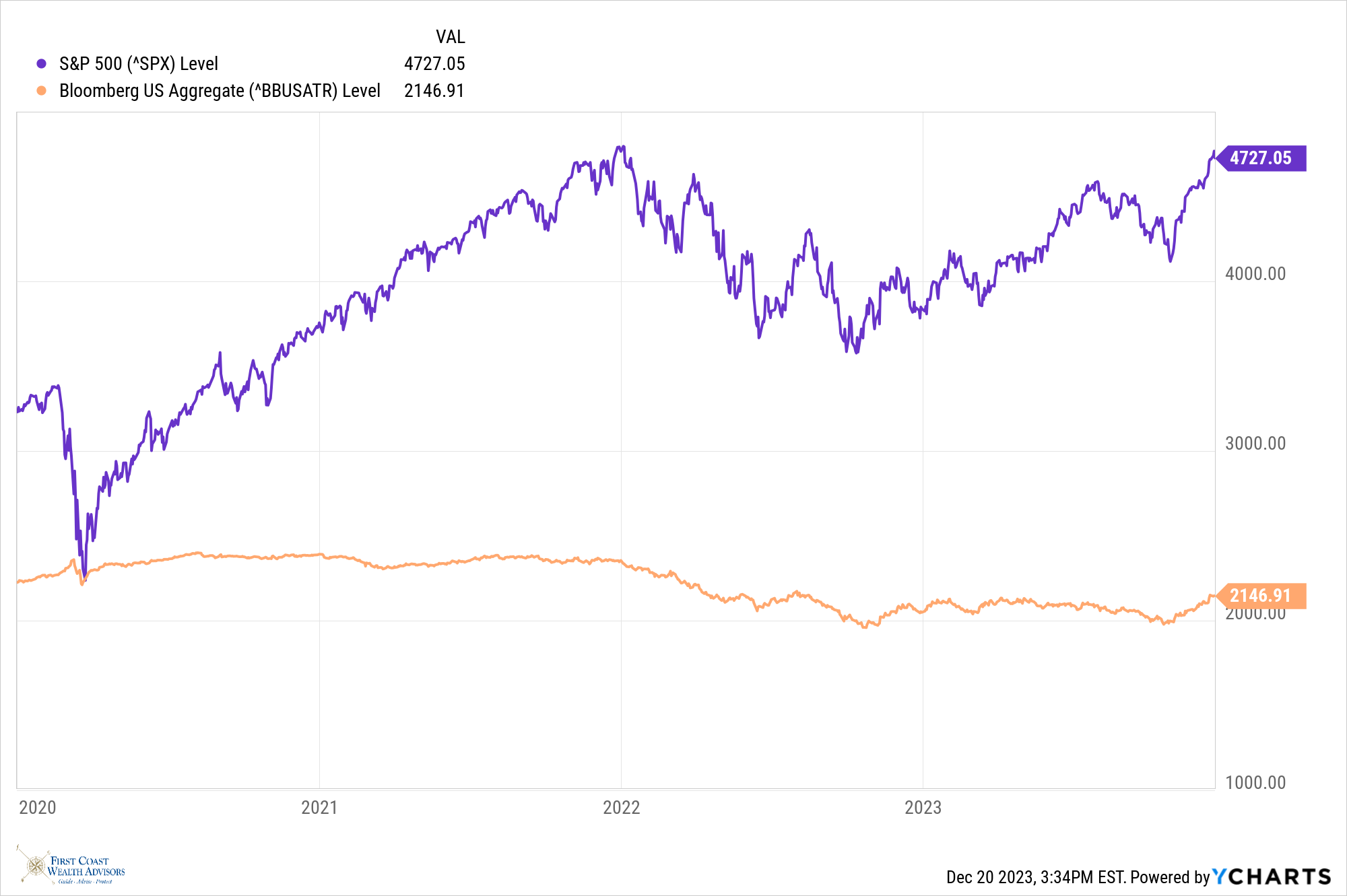

By March 23, 2020, the S&P 500 index, a benchmark representing the 500 largest publicly traded companies in America, was down more than 30%! Governments around the world closed their economies for what was supposed to be “two weeks to slow the spread,” but for many, it turned out to be two years. Unemployment peaked a month later at 14.7%. The next 18 months saw more than $7 TRILLION DOLLARS injected into our economy through a variety of stimulus packages that, for many, buffeted the effects of unemployment and lost wages, but for most who received it only bolstered their balance sheets. This led to rampant consumer spending in the face of supply shortages that eventually fueled inflation like we hadn’t seen in 40 years! Corporate profits for those 500 companies reached an all-time high, and on January 2, 2022, the S&P peaked with a gain of more than 48% since 2019.

If only the chain of events had stopped here. But no, we had to deal with the inflation that came from all that money circulating in the economy. While inflation peaked in June of 2022 just shy of 9%, the Federal Reserve spent the whole year increasing short-term interest rates at the fastest pace on record. What was 0% in January was 4.25% in December and would continue to increase to 5.5% in 2023. This incredible increase in interest rates resulted in the U.S. bond market suffering its worst performance in more than 100 years! For investors, this meant giving back a year and a half of gains.

Which brings us to 2023. Everyone is back to work, even if they are working remotely. There are still 1.2 job openings for every unemployed person. It’s normally the opposite of this. Wages have continued to increase around 5% per year – more for those at the lower end of the economic ladder. If you’re retired, you’ve seen your Social Security increase nearly 20% since 2019. Corporate profits have reached another new high. Inflation is trending toward 3% (which is the long-run normal state of things). And gas prices are lower today than they were in 2007! Oh, and the S&P 500 is about to eclipse its all-time high if it hasn’t done so by the time you’re reading this.

Takeaways

Any time you undergo a major shock to a system, like Covid, there are bound to be structural changes to that system that result. Our economy and financial markets are not immune to this. Here are five that I think are most important.

Remote Work is the new normal

The occupancy rate of commercial office buildings was nearly 100% before Covid. Since March 2020, the rate has struggled to exceed 50% in the nation’s ten largest metropolitan cities. Working in a hybrid fashion – where you’re in the office for a few days and remote for the rest – has become the new normal arrangement. It will likely take a recession for this dynamic to revert to the old way of working.

Inflation is back to 3%

Prior to 2008, the last significant shock to the system before Covid, inflation was trending at around 3% per year. The trend had been declining since the late 1970s when inflation peaked in the mid-teens. The period after the 2008 Financial meltdown was characterized by slow and modest growth, which kept inflation hovering around 1% per year. This was great news for consumers as it meant that interest rates on mortgages and auto loans were extremely low. But it was horrible for savers and investors because interest rates on CDs and bonds are tied together with inflation.

While it remains to be seen if the Federal Reserve will be able to achieve its goal of 2% inflation, consumers should prepare for a world where prices increase more each year than they did in the prior decade. The days of 3% mortgage rates are likely in the past.

For investors, this means things that are supposed to pay interest actually pay interest. We’ve spent a lot of time over the past year discussing interest rates on CDs and money market funds being back to pre-2008 levels. The yield on a 10-year government bond is around 4%, which is a good proxy for setting expectations on what bonds, as an asset class, will earn on an annualized basis over the next decade. 4% would certainly be better than the 1.2% earned over the last decade.

The U.S. stock market comes out of Covid increasing its dominance

U.S. stocks, as defined by the S&P 500 index, have beaten their international contemporaries in 13 of the last 16 years. So, what makes our stock market better than the rest? Simply put, we are the home of Innovation.

Companies that comprise our Tech and Tech-adjacent sectors make up 40% of the S&P 500. Love them or hate them, seven companies represent 1/3 of our stock market. The seven companies are Apple, Microsoft, Google, Amazon, Facebook, Tesla, and Nvidia. For context, Apple is worth more than the entire French economy. Add Microsoft, and you eclipse Germany. Collectively, these seven are worth almost all of China.

We often hear about how we “don’t make things in this country anymore”. That’s not true. We are the world’s innovators. Whether it was the invention of the integrated circuit in the 1970s or leading the development of AI today, I don’t see that changing any time soon.

Investor annualized returns should improve over the next decade

As I mentioned before, the return of bonds averaged a little more than 1% per year between 2008 and 2022. For the 30 years prior, the return was closer to 4.5% per year. In contrast, stocks have continued to average their historical 10% return. Diversified investors have experienced below-average returns for the past 15 years. The annualized return for an investor with ½ of their portfolio in stocks and ½ in bonds has been around 6%. Now that interest rates are back in their normal range, returns should be better than that over the next decade (of course, returns are not guaranteed).

Investors demonstrated they can handle temporary fluctuations

Perhaps the most notable observation to come from the Covid Era of investing is just how well-behaved investors – at least our clients – were during the experience. Essentially, nobody panicked during the 4 years of fluctuations. Almost everyone maintained their strategic long-term investment plan. A few increased their allocation to stocks. In general, investors maintained the best possible behavior during a period of unprecedented uncertainty.

If only they had more allocated to stocks along the way. The total return of a growth portfolio (70% U.S. stocks and 30% bonds) is 2X that of a conservative portfolio (40%, 60%) since January 1st, 2019.

Implications for tomorrow

What does all this mean for investors planning for, or living in, retirement? This question has been on my mind a lot lately.

For starters, I think it’s important to recognize the impact a normal rate of inflation will have on people’s #1 financial goal – don’t run out of money before running out of time. If inflation averages 3% per year over the next decade, that will be 2.5X more than we’ve experienced over the last one. The cost of living will increase faster than we’re accustomed to. Our income and assets will need to increase at an equal or faster rate just to keep up with the rising cost of living.

Some of you may be thinking about taxes and how they will change in the future. The $7 trillion that was put into the economy during Covid wasn’t paid for out of tax receipts. It had to be borrowed. Paying that money back is less of a big deal when the interest rate is 0% than it is when rates are now more than 5%. Our nation’s interest expense is set to top $1 trillion dollars this fiscal year! Eventually, this will have to be addressed. Couple this with the fact that our current tax policy is scheduled to sunset at the end of 2025, and you have the makings of a real possibility all of our taxes will go up. For the first time in my career, increasing tax rates is a possibility on my radar.

Which brings me to my final point. The only way to outrun inflation and taxes over the long run is to own more of the stuff that has the potential to grow in value. I know one of my observations suggests that returns for all diversified portfolios will likely be better over the next decade, but if you didn’t misbehave during the past 4 years, perhaps you can stand a little more of the stuff that is focused on growth. There has rarely ever been a time when a portfolio with more stocks than bonds didn’t grow more over a decade or longer.

If you have questions about your investment or retirement plan, please contact me. I and the rest of the team are here to empower you toward achieving your goals. Here’s to 2024.

The S&P 500 index is an unmanaged index of the 500 largest stocks in the United States based on their market capitalization. Investors can not invest directly in the index.