As we enter the dog days of a very different summer, we felt compelled to follow up our last commentary with an update on the state of things. We normally resist bombarding you with charts and graphs as you can get your daily dose of them from the news and social media. We’re going to make an exception today and share a few we think matter to answer questions that are on our readers minds. Specifically, what’s causing the disappointing spike in COVID cases, how’s the average household doing financially, and what’s in store for markets?

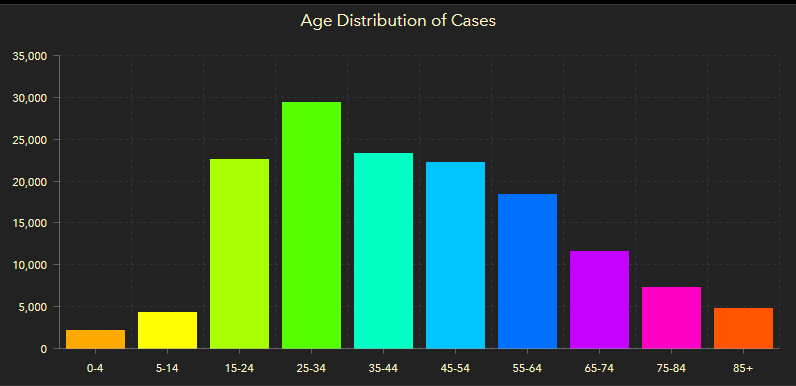

As you’re no doubt aware by now, the master plan to phase in the reopening of the economy has been met with a disappointing rise the number of positive COVID cases in states that began relaxing their containment efforts in late May and early June. While not unexpected, the rise in cases – particularly among the younger population – has exceeded the expectations of state and local leaders and public healthcare professionals. It’s impossible to determine exactly how much of the spike is attributable to increased testing versus increased person-to-person transmission. Both are certainly contributing to the result. Of one thing we’re sure: The re-opening of bars, restaurants, and beaches coupled with numerous public protests is certainly contributing to transmission spikes. The chart below from the Florida Dept of Health reflects the rise in new Florida cases from ages 15-34. Translation: These are the folks most likely to relax social distancing practices due to the easing of public closures.

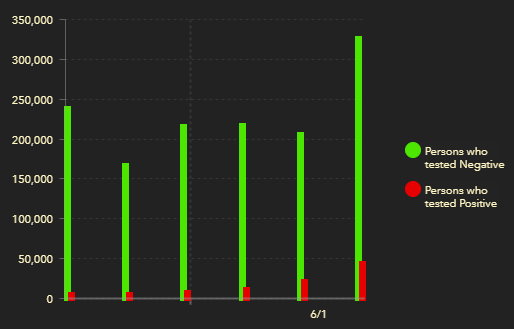

While we wouldn’t call it a bright spot, we can see that a meaningful number of new positive cases are coming from increased testing:

While the rise in positive cases is worrisome, some perspective is needed. First, many of those testing positive are asymptomatic – they aren’t hospitalized. They’re (hopefully) self-quarantining and will recover without treatment if they have any symptoms at all. Second, the number of hospitalizations in Florida is on the decline over the past few days. Last week’s daily high was 249; On June 28th, it was 110. Fatalities are also declining, down from 65 on June 22nd to 28 on June 28th. Those trend lines are important if they continue. In our view, watching hospitalization and fatality trends is more important than the new case stats.

As for what the next few weeks will bring, we can’t offer any insights. No one really can. The recent mandates for masks to be worn in public places should contribute to a leveling off and decline. We will see. If everyone simply follows the distancing protocols, things will improve far more quickly.

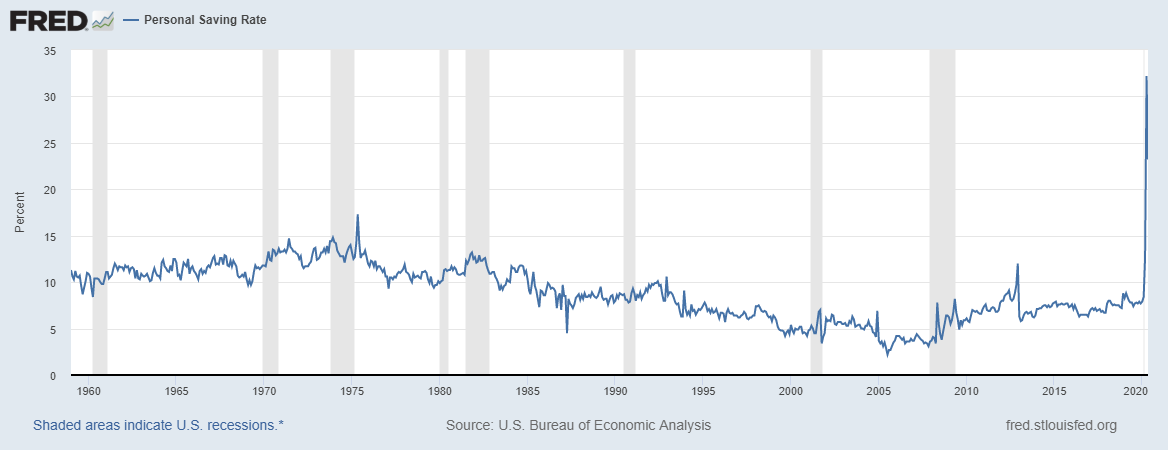

Shifting gears, we’re closely watching the economic metrics to determine how the gradual reopening of the economy is unfolding. Specifically, we’ve been interested in savings rates, household debt, and the timely payment of bills. These are good indicators of how households are faring. Let’s look at savings rates first. Household savings rates increased dramatically. (This isn’t completely unexpected, as there’s few places to actually go and spend money.) But the rate of savings is really unprecedented. Take a look at the spike in savings rates in 2020 according to the Bureau of Economic Analysis below. (Look all the way to the right side of the chart)

Translation: Households are stockpiling savings due to the ongoing uncertainties of the pandemic.

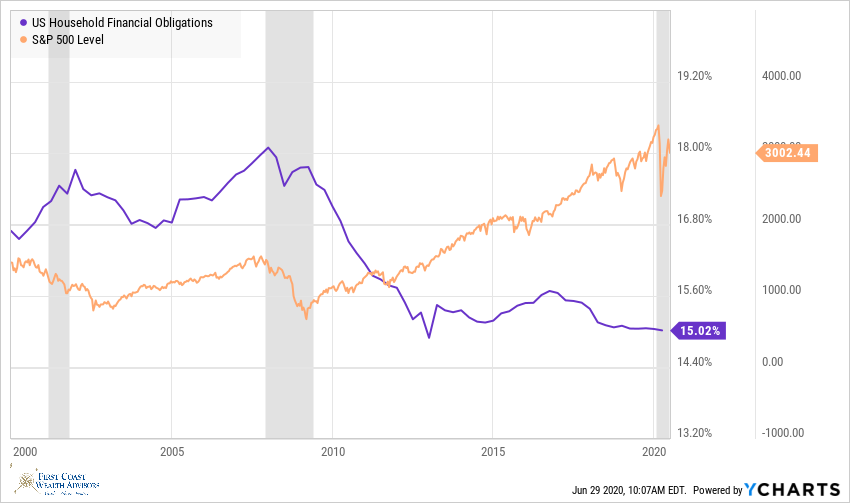

Regarding the dramatic rise in unemployment, one might think that defaults on consumer debt such as vehicle loans, credit cards or mortgages would be on the rise, but the data isn’t showing that occurring – yet. The S&P/Experian First Mortgage Default Index’s latest reading, as recently as May 30th, stands at 0.52% compared to 0.59% for the same period last year. Total household debt service, currently at 15%, show a similar story virtually unchanged from a year ago. (The blue line on the chart below)

You’ll note that household debt rates are significantly below peak levels seen in 2008. It’s likely the massive unemployment benefits provided by the Federal government and states, along with accommodative creditors are keeping these ratios in check. But the $600 weekly boost from the Feds is set to end on July 31st. In sum, households have continued to pay their debts despite the daunting unemployment numbers. Will we begin to see a rise in the level of defaults once the benefits end? Time will tell.

As for the investment markets, they have continued to show impressive resilience given the overwhelmingly negative news narrative. We believe markets will continue to show a “two steps forward, one step back” pattern similar to what we saw coming out of the 2008 financial crisis. The next few weeks will be critical in terms of the how the COVID numbers nationwide behave. If we see patterns of stabilization and decline similar to New York, Italy, and other early hotspots, we would expect markets to reflect it. If the data goes the other direction, markets will likely exhibit the same volatility (both up and down) we’ve become accustomed to over the past three months.

Our advice to investors remains the same: If you’re properly diversified for your long-term goals, stand fast. We encourage you to look at places like Italy and New York, formerly hotspots for COVID. New York practiced proper protocols and has seen their daily new case count drop from 11,500 in mid-April to 600 on June 27th. Italy? 6,500 daily new cases in late March to just 174 yesterday. This proves that COVID is containable if distancing procedures and health protocols are followed by the public. In addition, here’s the latest release from our friends at First Trust on the pandemic results and economic positives.

As for us, we’re in the office, practicing all the recommended protocols. If you have any questions or concerns, don’t hesitate to call. We’ll keep you updated as things progress.

Your First Coast Wealth Advisors Team