When it comes to saving for retirement, there are two ways to do it. You can either make pre-tax contributions to a Traditional account or after-tax contributions to a Roth account. In this context, I am referring to using a 401k or similar employer-sponsored retirement plan, but the concepts are the same for IRAs. The two types of accounts are similar in some ways, but their differences may lead you to favor one over the other. Conventional wisdom suggests the tax-free nature of withdrawals from Roth accounts makes them the superior choice. As you’ll see in this analysis, conventional wisdom might not be the best when selecting which type of account to contribute your retirement savings to.

Traditional and Roth accounts get different tax treatment

Traditional retirement accounts allow savers to make contributions on a pre-tax basis. The advantages of pre-tax contributions are twofold. First, contributions reduce taxable income in the year the contributions are made. And second, 100% of the contribution goes to work toward your retirement goal. Taxes on the contributions, and investment growth, are not paid until funds are withdrawn in retirement.

Withdrawals eventually must be taken from Traditional accounts. The IRS mandates that a minimum amount of withdrawals be taken upon turning 72; this is known as the Required Minimum Distribution or RMD for short. The government must collect taxes on those contributions and gains at some point, and they’d prefer to do it while you’re living.

In contrast, Roth accounts allow savers to make contributions on an after-tax basis. In exchange for paying taxes on your contribution today, the IRS allows contributions and investment gains to grow tax-free. Withdrawals taken during retirement do not incur any taxation. Unlike Traditional accounts, there are no mandatory withdrawals during retirement.

Pay taxes now or later?

Our federal income tax system is progressive in that as your taxable income increases, the tax rate you pay on that income increases too. Taxable income is the income left over after pre-tax deductions to employer-sponsored retirement and benefit plans and your standard deduction.

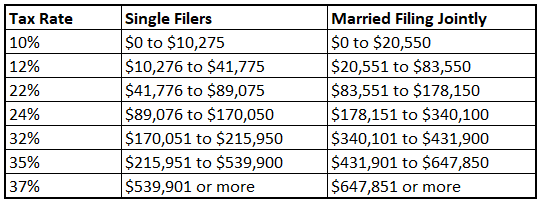

Under current law, there are seven marginal tax brackets. As your taxable income exceeds these margins, income at the next level is taxed at the higher marginal rate.

An example: An average married couple with a combined taxable income of $97,000 will find they are in the 22% marginal bracket. The couple will owe $12,574 in federal income tax. The first $20,550 of their income is taxed 10%, or $2,055. The next $63,000 up to $83,550 is taxed 12%, or $7,560, And the final $13,450 up to $97,000 is tax 22%, or $2,959. ($2,055 + $7,560 + $2,959 = $12,574.)

Marginal tax rates are only part of the story, though. A second tax rate is also important, and that is your effective tax rate. Your effective tax rate is the percentage of your total income you pay in federal income taxes, total income equal to all of your income before any deductions.

Example continued: the only deduction the married couple had was the $25,900 standard deduction they were entitled to when they filed their tax return. Their combined total income is $122,900. ($97,000 + $25,900 = $122,900). Their effective tax rate is 10.2% ($12,574 / $122,900 = 0.102) In this example, while the married couple is in the 22% marginal tax bracket, their effective tax rate is only 10.2%.

Understanding the distinction between marginal and effective tax rates is crucial to deciding which type of account you should contribute to. Since retirement contributions can reduce your taxable income, they are affected by the marginal tax bracket you find yourself in. If you are in the 22% bracket, any pre-tax contribution you make is essentially avoiding a 22% tax bill on that income today. Eventually, the day will come when a withdrawal is made, and taxes will be due on the amount withdrawn. As I’ve shown, the tax rate you actually pay is what matters. If your effective tax rate at the time of the withdrawal is 10.2% (using our example), you would have saved more than 50% on your tax bill for that pre-tax contribution.

Had you chosen a Roth account, you would not have been able to enjoy the immediate tax break, and you would have had to pay the marginal tax rate on the contribution before depositing it into your account. Withdrawals, including gains, will be tax-free in the future, but would it have been worth it? We’ll look at that in a moment.

The upshot is this: if your effective tax rate in retirement will be lower than your marginal rate today, pre-tax contributions are the way to go. If you think your effective rate will be higher in retirement than your marginal rate today, Roth contributions are the way to go. The higher your marginal tax bracket, the more beneficial pre-tax contributions are.

Aren’t taxes going up in the future?

I’ve heard this question for as long as I’ve been a financial planner (23 years), and guess what? While marginal tax brackets have fluctuated over time, effective tax rates have remained consistently around 12% for most taxpayers. Setting aside the political reason for this, the primary reason effective tax rates have remained consistent since the 1970s is that marginal tax brackets and deductions are adjusted for inflation. As inflation increases over time, the values that bookend the marginal brackets and the amount allowed for deductions have also increased. The net effect of these inflation-adjusted values means the average taxpayer will see their effective tax rate stay pretty steady (low) over time.

Will taxes go up in the future? While marginal tax rates might go up in time (current law has them reverting to 2016 levels in 2026), effective tax rates will likely not change much over time. As a financial planner, I prefer to make decisions based on facts rather than conjecture.

Would you rather have more wealth or pay less tax?

You may have noticed that I emphasized the tax savings on the initial contributions to pre-tax accounts while mentioning that withdrawals (in total) are tax-free from Roth accounts. The gains that accrue in pre-tax accounts will be taxed when they are withdrawn in the future. Unlike Roth accounts, gains are not tax-free, just tax-deferred. Making pre-tax contributions has the genuine possibility of you paying more income taxes over your lifetime than had you contributed to a Roth account. Would you accumulate less wealth over time due to paying more tax? Not necessarily.

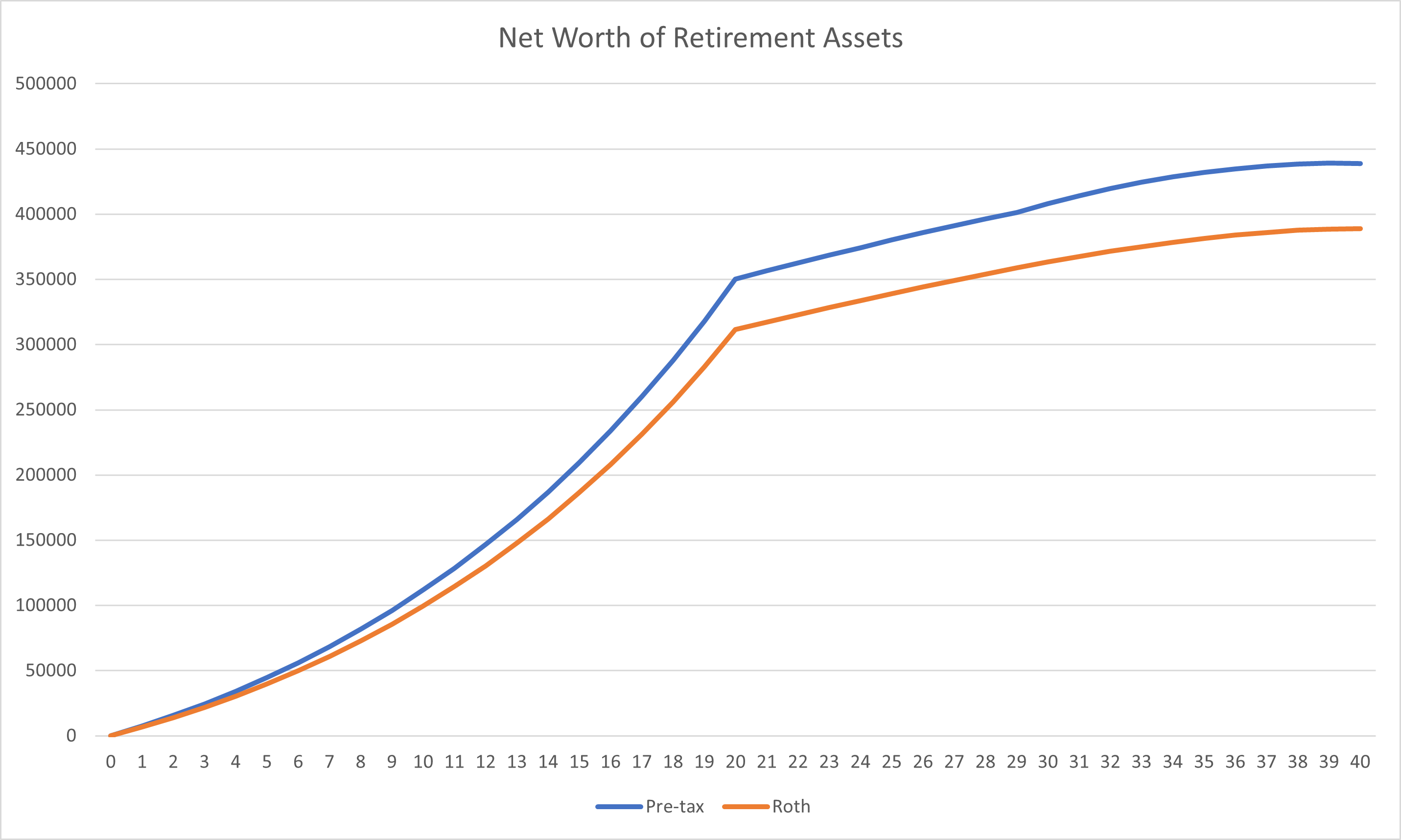

Given enough time, pre-tax contributions will accrue more net worth than Roth contributions, even after accounting for the prospect of more lifetime taxes.

For example, a single retirement saver aged 40 making a gross income of $75,000 chooses to contribute 10% of her pay toward retirement for the next 20 years. Inflation is expected to average 3% per year with a reasonable 6% annual return on her investments. Tax rates are expected to remain constant.

The pre-tax contribution during the first year would be $7,500, and the Roth contribution would be $6,672 after paying taxes. That difference in contributions favors the pre-tax option, and you’ve got more working out of the gate without the tax drag.

At the end of 20 years, the pre-tax account had accumulated $350,256, while the Roth account grew to $311,588. Choosing to make Roth contributions meant you would have paid an extra $22,249 in taxes along the way.

Withdrawals begin at age 66. A safe withdrawal percentage from a pre-tax account in year 1 of retirement is 4%. Starting at this withdrawal rate will allow for cost-of-living increases through retirement without jeopardizing the account’s longevity. After paying taxes, she is left with a spendable amount. We’ll use that spendable amount in the Roth comparison to keep things fair. In year 1, the withdrawal from the pre-tax account is $14,010. After taxes, the spendable amount is $12,329. That’s the amount that would come from the Roth account.

For the next 19 years (through age 84), annual withdrawals increase to keep up with inflation. Beginning at age 72, a minimum distribution is required from the pre-tax account, assuming regular withdrawals are not above a certain level. The Roth account has an advantage here since the IRS does not require minimum distributions from them.

Assuming she passes in her twentieth year of retirement, her pre-tax account would have grown to $438,967, while the Roth account would have only grown to $388,983. And that’s after having paid $45,175 in taxes on the pre-tax account withdrawals. In the end, the pre-tax account is nearly $50,000 larger despite having paid twice as much income tax over the 40 years.

Would you rather accumulate more wealth over your life or pay less income tax? All else being equal, I would rather accumulate more wealth.

Factors that make this possible

Two variables make the advantages of Traditional pre-tax accounts possible.

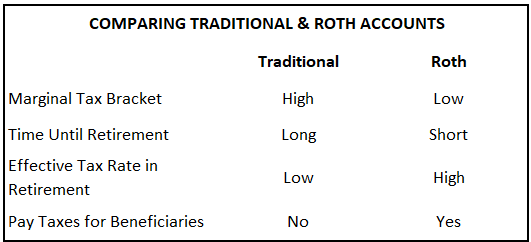

First, the higher your marginal income tax rate during accumulation, the larger the benefit will be from a Traditional account. If you are in the 10 or 12 percent marginal tax bracket, contributing to a Traditional account will still accrue more wealth over time, but the difference compared to a Roth account will not be significant. That’s because your effective tax rate will likely be close to your marginal tax rate.

Second, the longer the timeline until retirement, the more pronounced the difference between Traditional and Roth values will become. The scenario I used in this article assumed a twenty-year accumulation period. The power of compounding the tax deferral is only possible if enough time is allowed to pass. As the timeline shortens, the difference between the two types of accounts diminishes.

Wrapping up this discussion

The economic advantages of Traditional accounts should be clear. However, there is one reason Roth accounts might be preferable. I’ve only come across this once before. In that case, the client wanted to pay the taxes instead of having their children do it upon inheritance. As such, they chose to forgo the economic benefit of Traditional accounts and made Roth contributions so their kids wouldn’t have to worry about the taxes later.

I put this guide together to help in decision-making. Hopefully, you find it helpful.

If you have any questions about this, please reach out. I would be happy to discuss how this applies to your specific situation.

By the way, the financial markets have been very challenging this year and we understand how difficult it can be to stay focused with your investment plan. Fortunately, pull backs like the one we are experiencing this year are rare and often lead to outsized returns in the year that follows. Check out our article on how history has played out before.